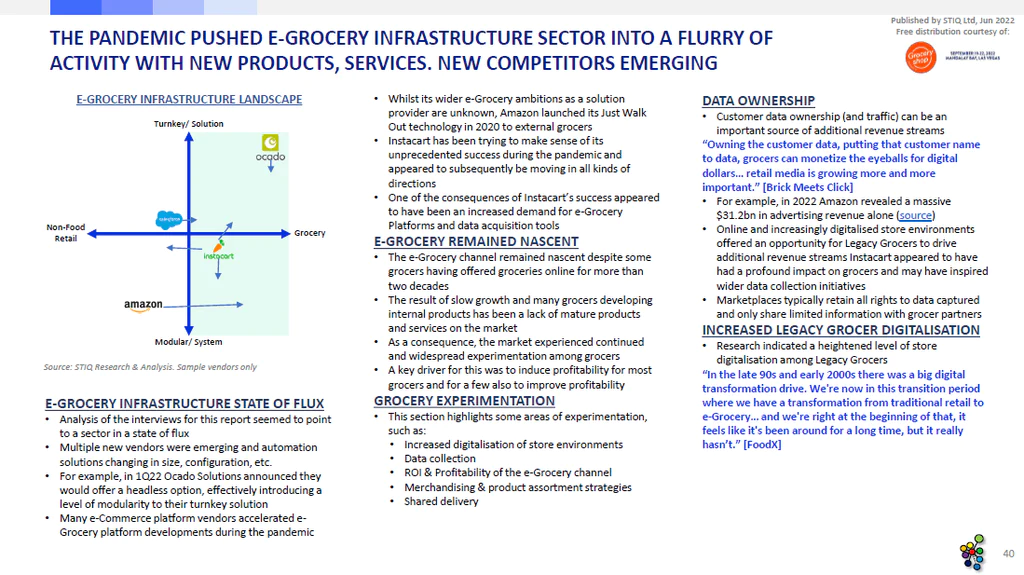

Non-legacy grocers very active buyers of material handling automation equipment

Increased traction for e-grocery platforms and headless architecture is now preferred option

Early mfc adopters continuing deployments

The first multi grocer locker delivery network

Neutral

Multiple material handling system integrators have hired snr automation people from grocers; e-grocery viewed as the next big trend after e-commerce

Mfcs no longer viewed as a silver bullet, network approach from top warehouse automation vendors

Multiple new vendors; legacy vendors have released products & services overlapping with e-grocery

Negatives

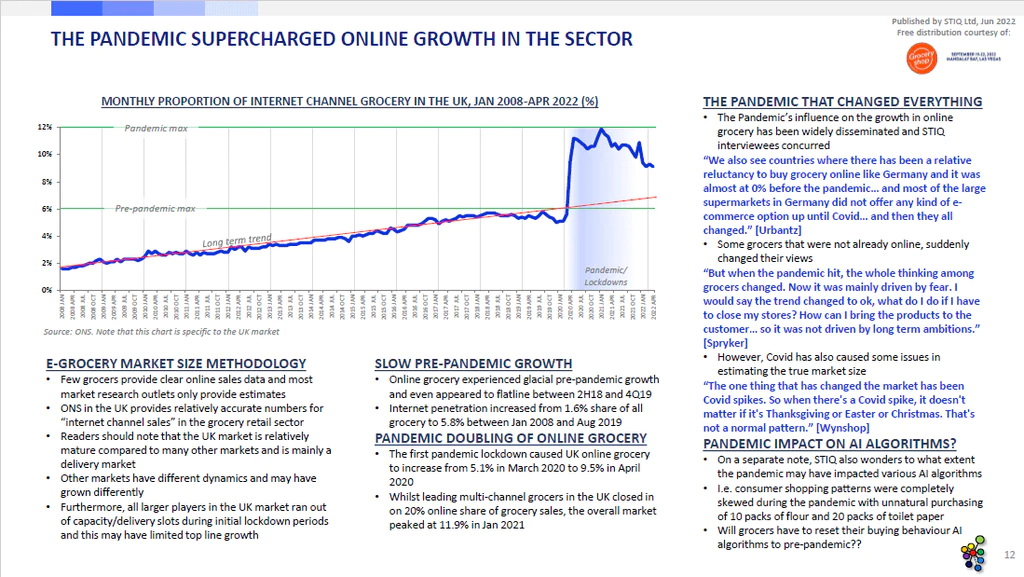

Online grocery sales declining from pandemic highs; declines at different speeds and likely influenced by geopolitical events & surging inflation

The partnering trend between mfc + e-grocery platform vendors has cooled/died

New mfc customer deployments quiet since the 2021 e grocery infrastructure report

Grocery sector extremely complex

Stiq acknowledges that the grocery sector is extremely complex with often short or immediate supply chains from farms to stores, often difficult to replicate

Many pureplay online grocers have partnered with legacy grocers for ready made supply chains

Online grocery sales remain at <10% as a proportion of all grocery sales in many countries, even strong online countries, such as the uk

Post pandemic impact, inflation

Many publicly traded grocers have announced expanded capex on digital & online initiatives and stiqs view is inflation will not affect the sector in the short term

However, there may be continued supply chain challenges for robotics and other automation equipment

Pandemic effects are subsiding fast and it is difficult to estimate any permanent positive effects on sales

Furthermore, post pandemic inflation caused by geopolitical events, qe, etc. Is currently impacting consumer behaviour

Clear differences in 2022 interviews

Stiq noticed a number of clear differences from the 2021 report (download here for free)

The main difference was the lack of new mfc deployments + a sense that legacy grocers (those with stores) are taking time to consider their approach to the online channel

Part of this could also be that many grocers built up significant technical debt during the pandemic that they are now unravelling

Significant experimentation

Grocers are experimenting significantly across online grocery technologies and modalities

For example, the very first shared (multi legacy grocer) last mile solution was unveiled in paris in 2022

No silver bullet

Overwhelmingly, stiqs impression of 50+ interviews and conversations with industry participants is that the sector remains in its infancy despite pr initiatives by early adopters and technology vendors

Significant hiring from grocers including such warehouse automation teams hints that vendors have some expectation of larger projects to come

Whilst legacy grocers have been relatively slow to buy equipment, pureplay grocers have accelerated automation deployments to gain and retain market share

This report is available free of charge thanks to the generous sponsorship of Grocery shop

Grab Your Free Report

Would you like a full report on the latest trends in mobile robotics with unique insights directly from the main vendors in the space?