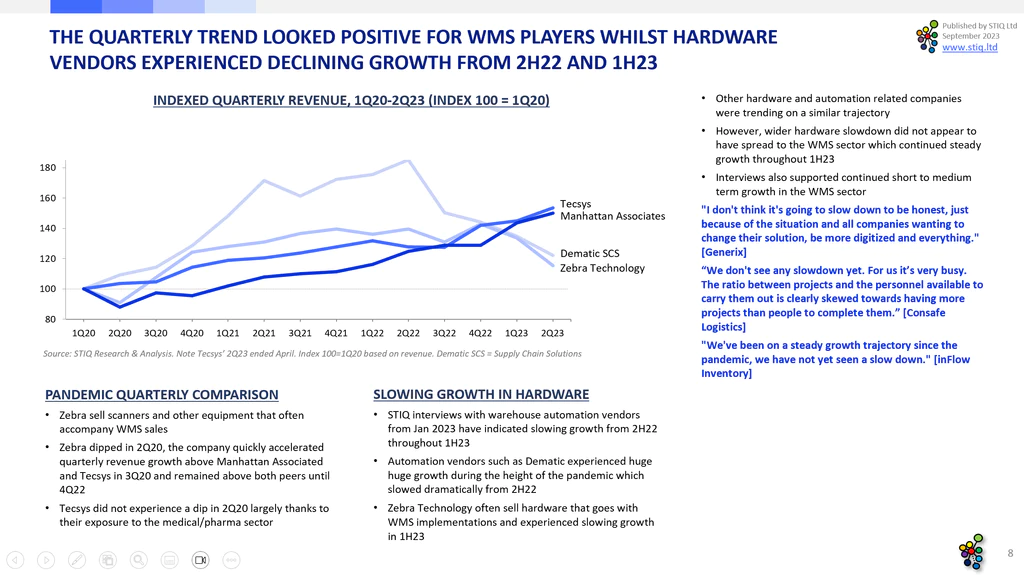

Strong continued WMS sector growth isolated from current automation sector challenges. Access to experienced staff, a growth limiter.

Most WMS vendors interviewed for this report indicated very healthy growth in 2023, continuing a

longer-term sector trend.

WCS and WES vendors reported somewhat muted growth in 2023, primarily as these solutions often

follow trends in automation hardware where there has been some headwinds in 1H23.

Primary drivers of demand include a continued switch towards multi- and omni-channel, wider

cloud adoption and supply chain resilience.

Interviews suggested higher growth could have been achieved but for a lack of experienced

logisticians with WMS knowledge.

Vendors expressed a high level of confidence and optimism for short- to medium-term growth.

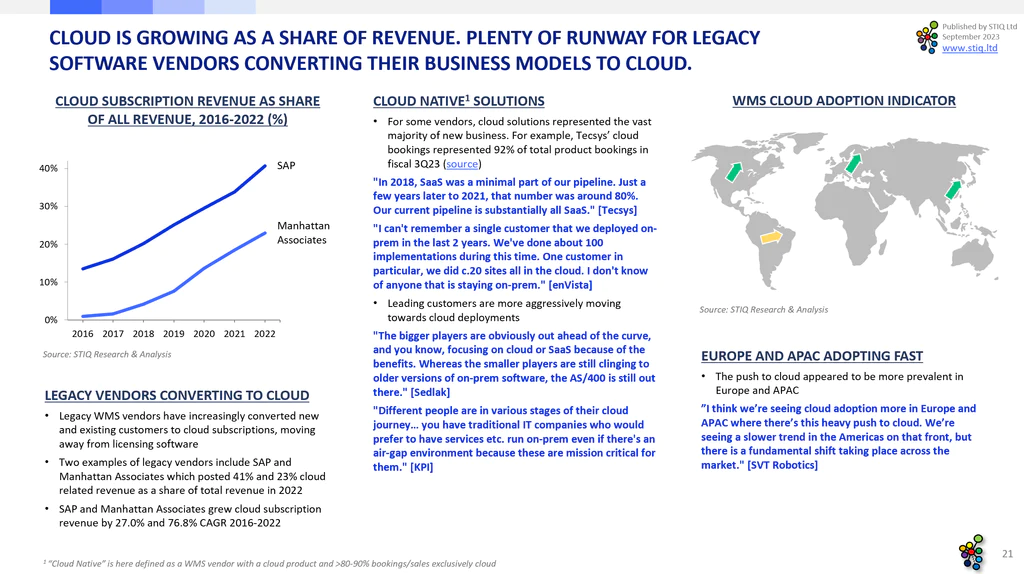

Continued appetite for WMS cloud deployments was viewed as a a key market driver.

Whilst the WMS sector has been late to the cloud, vendors highlighted healthy growth with an

increasing number of cloud native vendors.

Few industries required on-prem deployments and if so, often for security or compliance reasons.

Increasing geopolitical tensions may increase demand for on-prem or private cloud deployments.

WCS and WES solutions remained on-prem primarily due to potential latency issues.

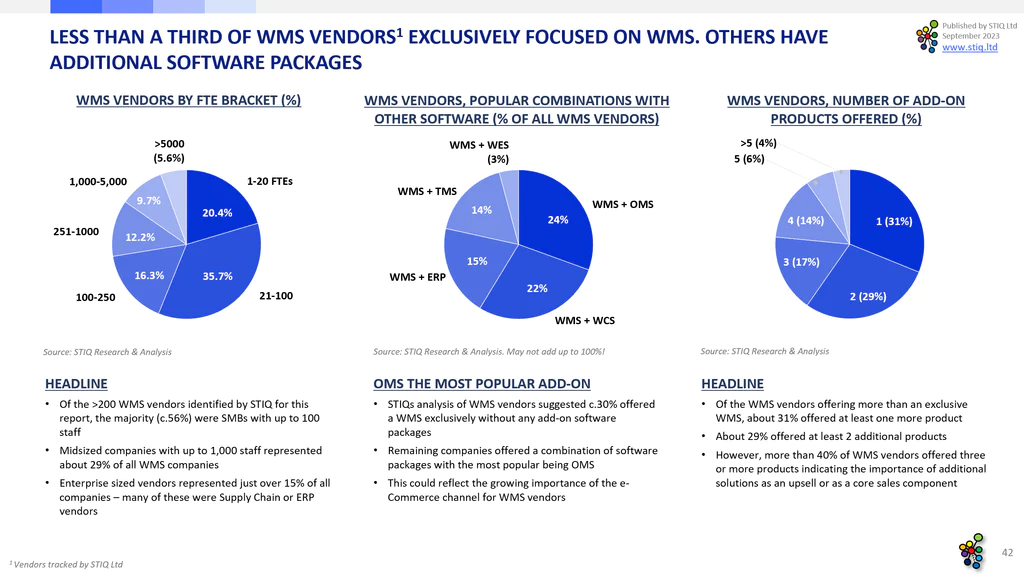

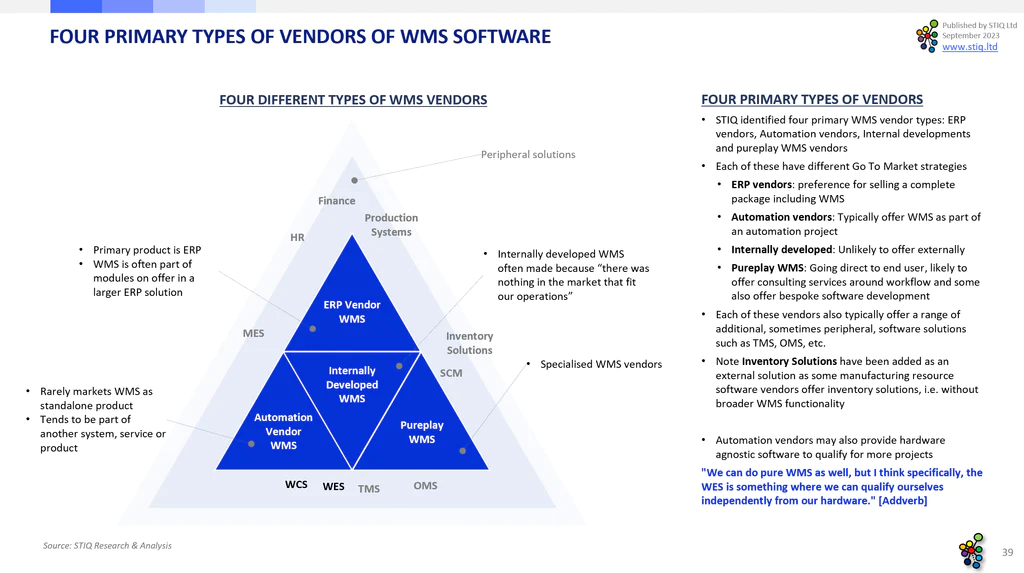

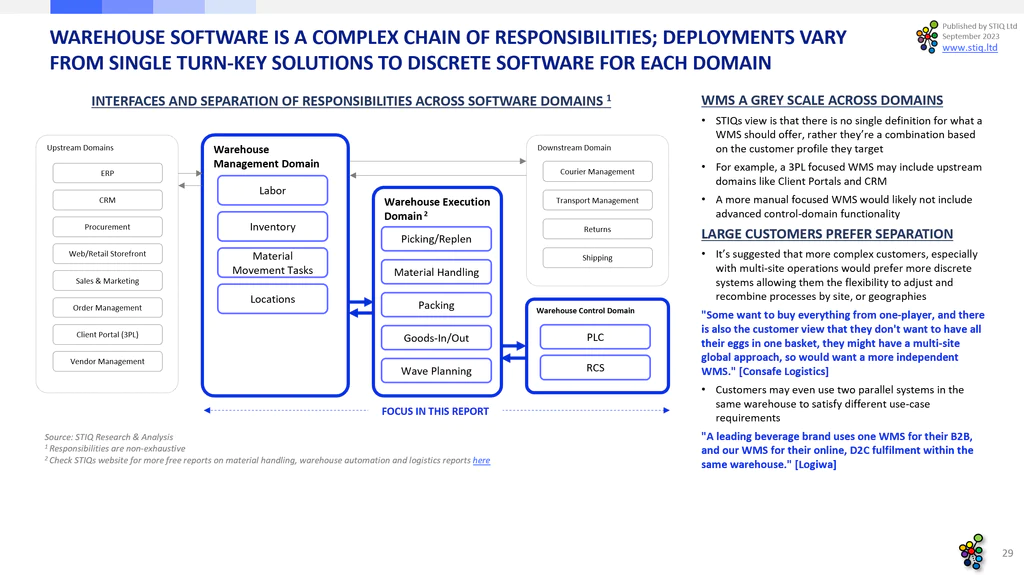

There was a wide range of different WMS vendors, from ERP companies to pureplay WMS businesses

and warehouse automation providers.

Many WMS vendors offer additional products and 31% of all vendors offered one additional software

product, the most popular being an OMS.

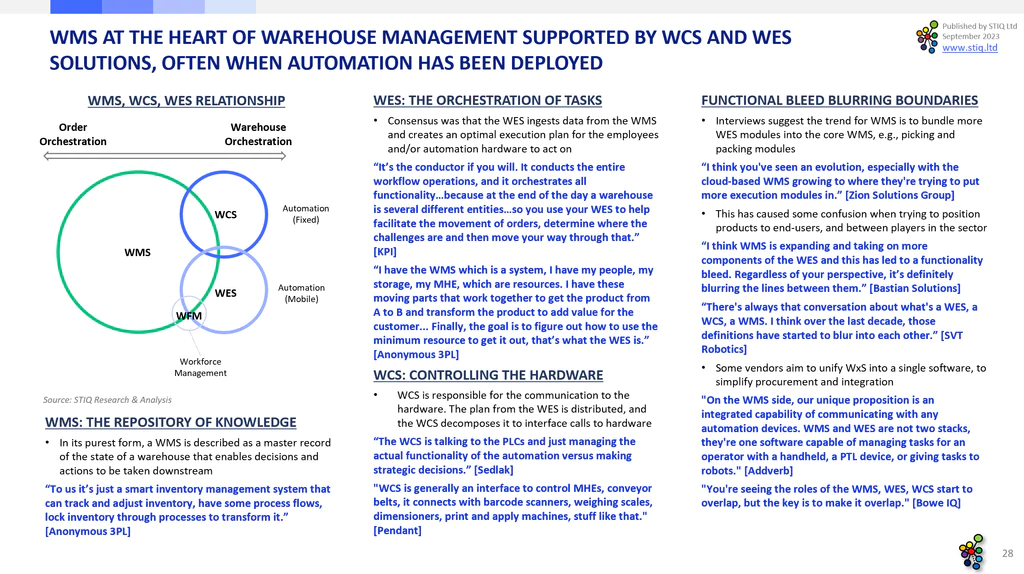

In recent years, the WES has emerged with a variety of definitions, but most often used in connection

with some form of automation, frequently robots.

Interviews suggested the WES could be a ‘missing link’ between the WMS and WCS, but also that WES

functionality has been around since early 2000’s.

Some WMS vendors suggested an increased use of warehouse automation in the medium to longer

term may have a detrimental impact on revenue growth with less seats/ users being needed.

Furthermore, often confusing and opaque pricing practices in the wider WMS sector has led to

younger players offering simpler pricing options.

The WMS software sector has experienced a relatively high level of M&A activity with 30

transactions since 2020.

STIQs research also indicated nearly a third of all vendors identified in the sector had been involved

in an M&A transaction.

This market report is available for free to members of the Mobile Robot Directory, thanks to our partnership with STIQ.