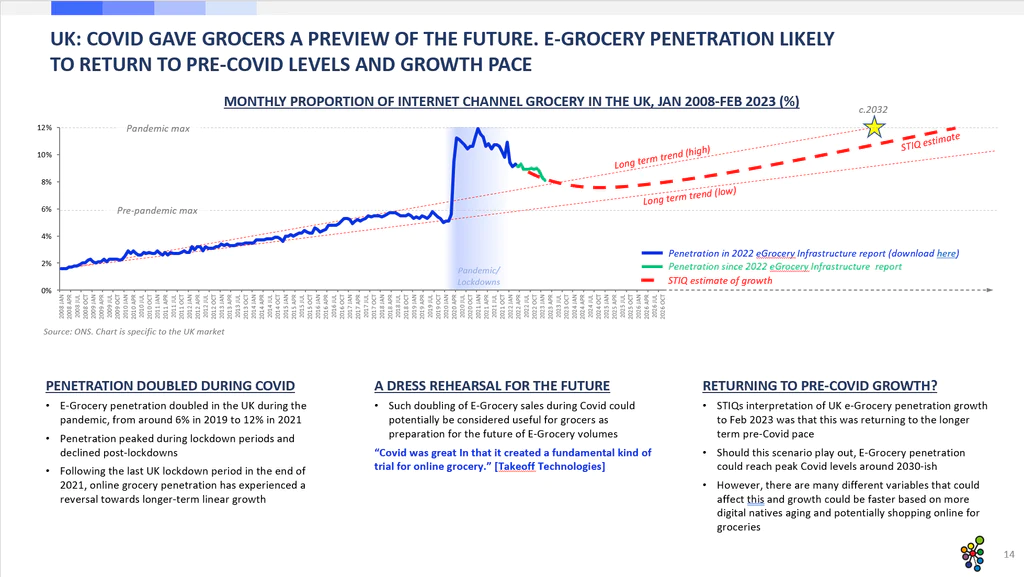

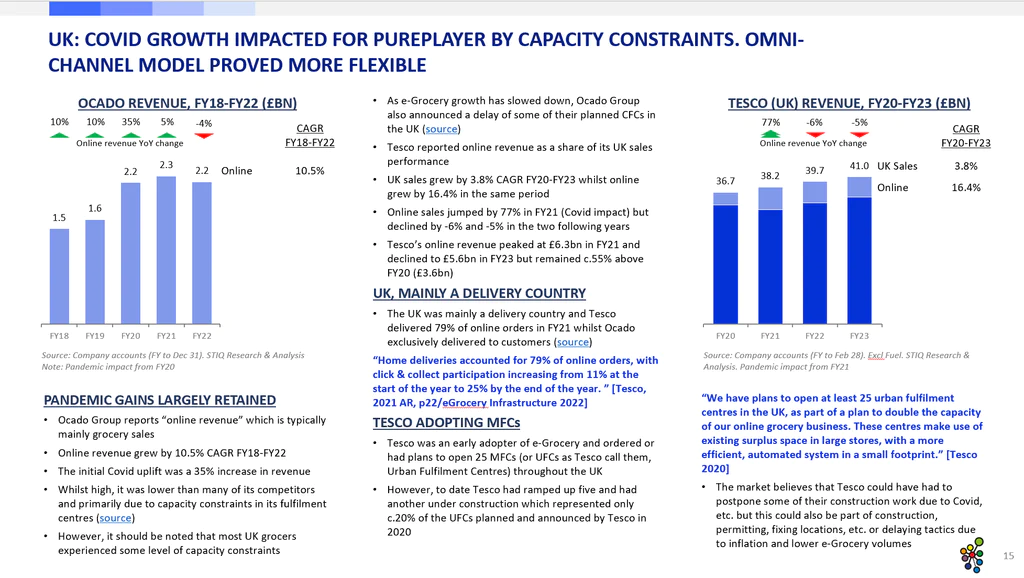

Post-covid grocers no longer capacity constrained. Covid was an “e-grocery future preview”, medium to long term positive for vendors

This market report is available for free to members of the Mobile Robot Directory, thanks to our partnership with STIQ.