The pandemic accelerated e grocery growth; lack of previous investments has led to a disparate & nascent vendor landscape

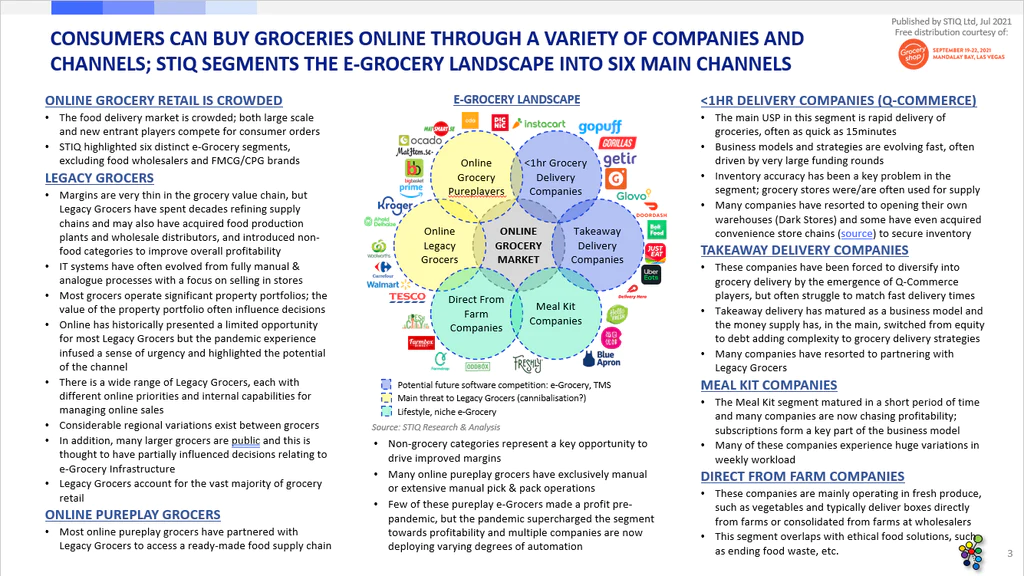

The grocery sector

Consumers have been able to buy groceries online since the late 1990’s, but traction remained muted compared to general e commerce

This lack of traction stemmed mainly from the structural heritage in the grocery sector, where the core focus was on stores/property portfolios, partnerships with fmcg/cpg and improving efficiencies in the supply chain

Adding to the structural inflexibility was low margin goods, three temperature zones, expiry dates, fragile goods, and large baskets (30 60 items)

As evidence of the inherent structural challenges in the grocery sector, many pureplay e grocers have partnered with legacy grocers to gain access to a supply chain

Amazon appeared to have acknowledged this with their $13.7bn acquisition of whole foods in 2017

Pandemic for grocers

Whilst the pandemic poured rocket fuel on online sales, very few legacy grocers actually surpassed 10% online as a share of revenue (only tesco reached above 10% online in fy2020 according to stiqs research)

Many online pureplay grocers experienced huge growth that, for a few, also exposed supply chain limitations, including access to more delivery vans, employees, etc.

In north america, instacart turned into an overnight sensation and possibly the top e grocer globally

Funding inflows increased with larger rounds mainly targeting new e grocery models, such as q commerce

Pandemic for vendors

In 1h20 most grocers froze, delayed or indefinitely postponed non critical projects; although many projects resumed in 2h20, there was a lack of new projects

In 1h21 e grocery infrastructure experienced increased m&a activity among software platforms, and acquisitions included locai , freshop and shophero

Whilst e grocery experienced huge growth, ecommerce also rocketed and mhe vendors serving both sectors reported healthy 2021 order books in h1, mainly from e commerce customers; one likely consequence was expanding lead times across the mhe sector

Interviews suggested that inquiries had increased and more vendors had decided to join the sector

E grocery infrastructure innovation

A major side effect of grocer’s lack of investments in e-grocery has been a highly sporadic technology vendor landscape with a majority of vendors also serving non-food retail (among other industry verticals) and there were very few vendors with proven end to end solutions

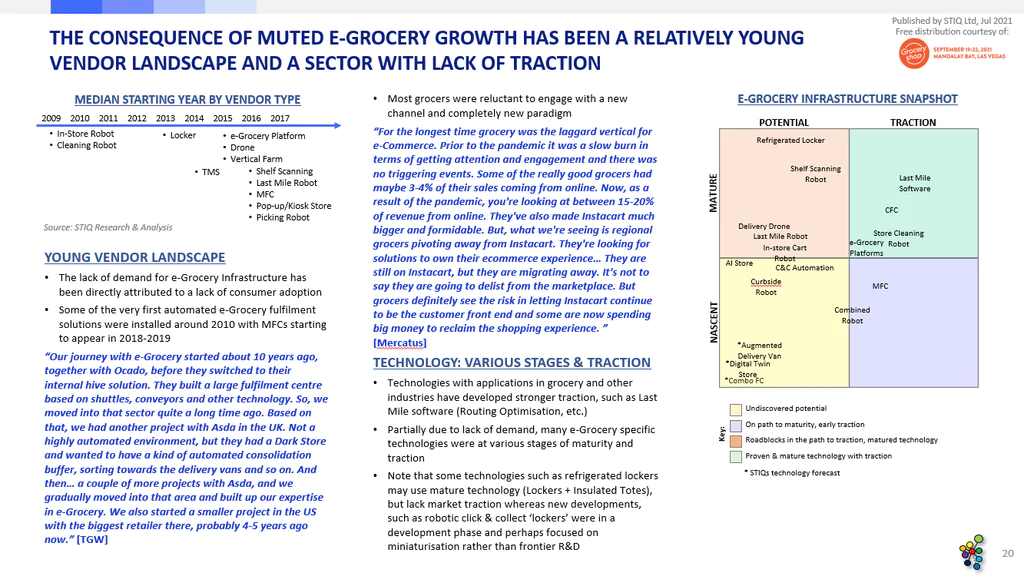

Whilst e grocery infrastructure startup activity increased in 2015 & 2016, prior to this, most r&d activity was mainly driven by grocer’s internal teams

Takeoff technologies first mfc went live in 2018/2019 and fuelled an intense, yet to be resolved, debate of where to fulfil e grocery orders centrally or locally

“potential” a key driver

Legacy grocers remained the target for larger investments and especially for mfc vendors that often cited large store estates as potential for growth

Pureplay e grocers were increasingly active buyers of e-grocery infrastructure

Barriers to growth

Interviews suggested a key barrier to further growth was legacy grocer’s roi expectations

However, the complexity of grocery retail was also often quoted; adding complex automation equipment to brick & mortar stores brings additional challenges; branding was also an important topic for many grocers, often preventing network effects

The future?

At the time of writing this report there was increasing interest in ‘amazon go’ technology… Potentially to focus on in store inventory accuracy, a well known problem

And, whilst many grocers were struggling with multi channel retail, axfood and alibaba freshippo were deploying omni channel capabilities

This report is available free of charge thanks to the generous sponsorship of Grocery shop

Grab Your Free Report

Would you like a full report on the latest trends in mobile robotics with unique insights directly from the main vendors in the space?